Don’t fool yourself: Gold is not an inflation hedge

A JPMorgan banker asked me many years ago what I would recommend as an inflation hedge. “Inflation-indexed bonds” was my first response, however I recanted that suggestion a few minutes later, noting that Inflation-indexed bonds still carried substantial real-interest rate exposure. Further reflection led me to suggest cash, since the cash-rate is targeted by Central Banks as their preferred tool for fighting inflation. Monetary policy is basically the following rule: cash-rates go up when inflation goes up and vice versa.

The banker was not impressed with the answer, since he would have preferred a funky derivative structure to recommend to his client. [I still stick by my view today – cash is a good proxy for inflation and current monetary policy wisdom ensures that cash rates go up with inflation and vice versa. ] “What about Gold?” asked the banker. Much to his surprise, I responded “Definitely not…”

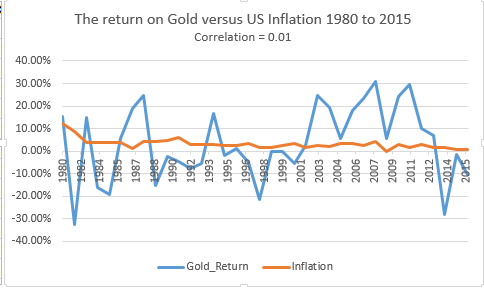

I am amazed at how investing folklore identifies Gold as an inflation hedge, despite the facts. Consider the following diagram which plots US Inflation in orange versus Gold return in blue, on an annual basis from 1980 to 2015.

If Gold were a perfect hedge for inflation, the blue line would sit smack on top of the orange line. The picture shows that nothing could be further from the truth. The volatility of Gold’s return is over 7 times that of the inflation rate. Nearly 1/2 of the Gold returns are negative (like, -30% negative in some years!) while inflation is always positive. The statistical correlation is 0.01 which means that the two quantities bear no resemblance to each other whatsoever. While its not obvious what is driving Gold returns to be so volatile, it’s pretty clear from the picture that its definitely NOT inflation holding the steering wheel.

I am strongly in favour of a Gold standard since, properly adhered to, it would discipline the monetary authorities to stop experimenting with policies like QE, and there would be less attention paid to the utterings of rock-star-like Central Bankers. But, in the absence of a formal link between Gold and the Money Supply, don’t expect Gold to automatically protect your portfolio from a loss in purchasing power.