Converting the annual rebalancing skeptics with a statistical Petri dish

Today’s post reports some research results that I am quite excited about. I must apologise that the research is motivated to help our potential investors better understand our investment process, so therefore it is an advertisement of sorts. Advertisements aside, you should find the results quite interesting.

Those of you who are familiar with our investment process for the First Degree Absolute Return Fund will know that we rebalance our strategy ONCE per year in March. This is radical and unique compared with all other managers. Radical investment ideas are often viewed with skepticism, which is fair enough, so it falls to the proponents to prove their case in as many ways as possible. Our meetings with potential investors generally go like this:

Skeptic: why do you rebalance once per year rather than more frequently like all other managers?

First Degree: the empirical evidence is irrefutable that forecast power for financial variables increases with the time horizon. If financial variables exhibit cyclical behaviour, with a periodicity of 5 to 10 years, then less frequent rebalancing synchronises the strategy to this cycle. Take our word for it!

Skeptic: Hmmmm…

Well, numbers speak louder than words, and pictures based on numbers speak louder still. The research I report today comes from a statistical laboratory where cause and effect are tightly controlled, internally consistent and fully transparent. The objective is to prove that if underlying decision variables, such as interest rates, exhibit cyclic behaviour and persistent shock with slower moving components then annual rebalancing will outperform more frequent rebalancing rules. The proof grows on our statistical Petri dish in 4 simple steps.

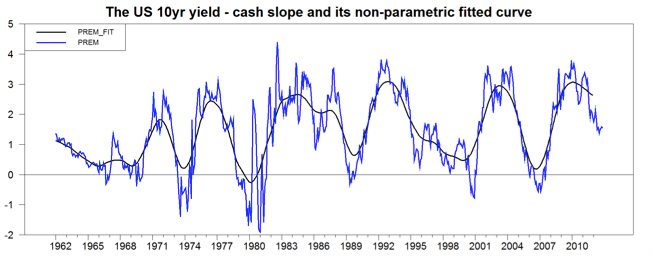

Step 1: Motivate the cyclical nature of interest rates with real data. The following picture displays the US 10yr yield minus the cash rate from 1962 to the present, together with a fitted curve.

This picture suggests some form of cycling in the 10 year minus cash yield.

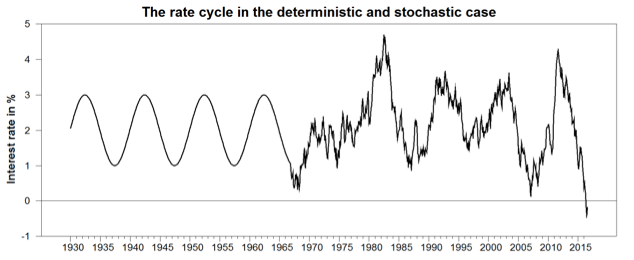

Step 2: Build a laboratory which generates cyclic and shock behaviour in the 10 year yield. The following diagram specifies a deterministic Sine curve for interest rates coupled with a peppering of persistent shocks to simulate risk.

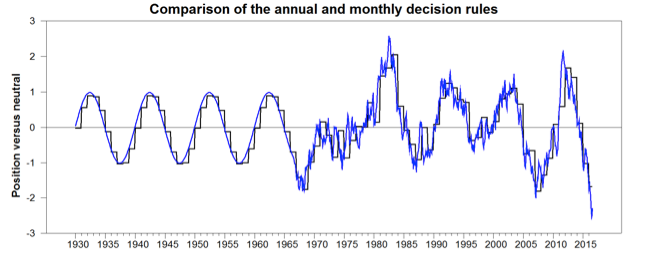

Step 3: Construct annual and monthly decision rules that depend on this interest rate behaviour to calculate relative performance of each

The step function is the annual rebalancing rule while the monthly rebalanced portfolio position taking is smoother.

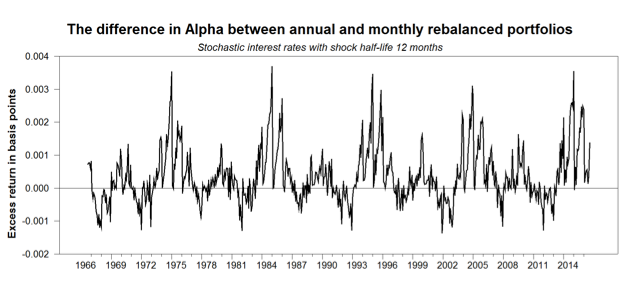

Step 4: Do this 1000 times and verify that the annual rebalancing rule outperforms the monthly.

This picture shows quite clearly that, on average, annual rebalancing outperforms monthly rebalancing rules. This is not always true, but the success rate is significantly greater than a coin toss.

Have I converted any skeptics out there? Access the full version of the research at our website at https://www.firstdegree.asia/assets/annual-triumphs-monthly-rebalancing.pdf