Meet the NEW real interest rate

In Japan, short term Tbills have a negative yield of -0.25% while inflation is negative -0.4%. The real interest rate is positve, roughly +0.15%.

In the US, short term Tbills have a positive yield of 0.25% while inflation is positive 1.0%. The real interest rate is negative, roughly -0.75%.

It may come as a surprise to some readers that real interest rates are higher in Japan than the US. Savers in Japan receive a positive real return while those in the US experience purchasing power erosion. This is not to say that US investors should pile into Yen cash (the exchange rate risk is high and exchange rates generally have a bad track record in reflecting relative inflation rates). But it does highlight the point that negative NOMINAL interest rates have attracted all the publicity recently, while negative REAL interest rates are just taken for granted and not worth a story. In fact, so common are negative real interest rates in the US that investors holding cash have suffered a cumulative 11.6% loss in purchasing power since 2008 while the Japanese cash holders have gained in purchasing power about 0.4% over the same period.

So while everyone pretty much accepts that real interest rates can be negative for extended periods of time, they are still getting used to the negative nominal interest rate phenomena. Negative nominal rates are therefore seen as desperate stimulus measures and unlikely to continue for an extended period of time. Accordingly, the bond markets, which have extrapolated negative rates forward into longer maturities, are seen as ‘dangerously overpriced’ and a ‘screaming short’ which no rational investor would enter voluntarily. But what if the nominal interest rate is actually reflecting the real interest rate market? Could this justify an extended period of negative nominal interest rates across the bulk of maturities?

The idea that the nominal interest rate is the NEW REAL INTEREST RATE has not caught on as yet, but the idea is worth contemplating. Simplistically, the nominal interest rate should equal the real interest rate plus inflation. This means that if inflation is expected to be zero for a long time, the nominal interest rate should equal the real interest rate (see footnote 1). It follows that if real rates are negative then nominal rates are negative too (see footnote 2).

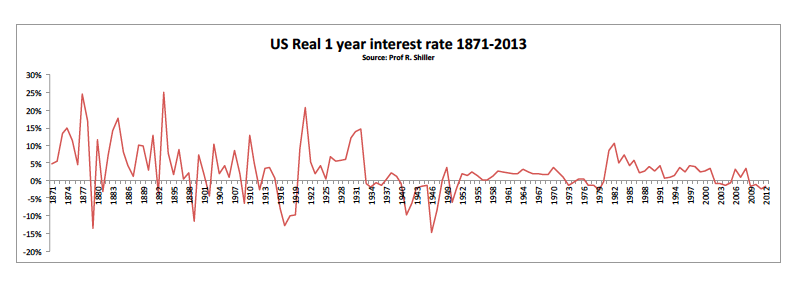

The point of this is that the world could be in for an extended period of negative nominal interest rates. The figure shows that the real 1 year interest rate in the US fell below zero for 4 or more consecutive years on 5 occasions since 1871. With inflation dead, the same may follow for nominal rates too.

Footnote 1. For the expected inflation rate to be zero for a long time, the monetary authorities either pursue a solidly disciplined monetary reduction policy or the transactions demand for money collapses. In the current environment, the latter would seem to be the most likely cause of an extended period of zero inflation.

Footnote 2. Yes, I know this violates an arbitrage condition, but let’s face it, nominal rates are negative in Europe and Japan.